Key Takeaways

Putting a price on everything quietly reshapes what society values

Carney's core thesis is alarming. Over centuries, economic theory shifted from objective value (rooted in production and labor, from Aristotle through Marx) to subjective value (price equals worth, from the neo-classicists onward). This shift was initially academic — but it escaped the textbook. Today, the logic of buying and selling governs healthcare allocation, education, environmental protection, even civic life. We've moved from a market economy to a market society.

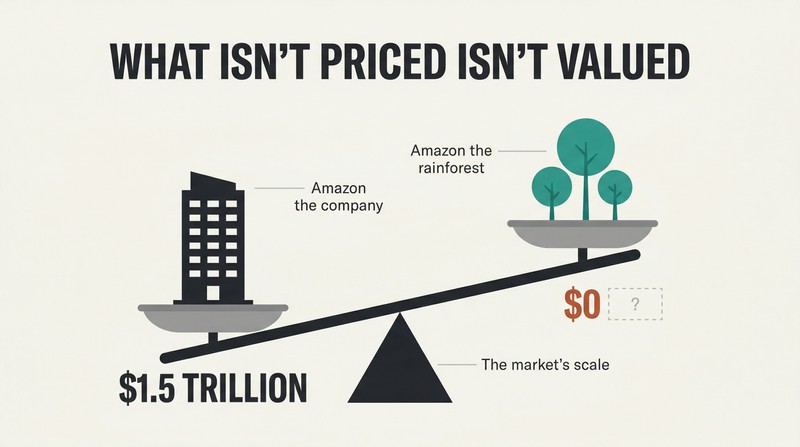

Consider the Amazon paradox. Amazon the company carries a $1.5 trillion valuation reflecting expected future profits. The Amazon rainforest — which regulates the global climate and harbors millions of species — appears on no ledger until it's stripped bare for cattle. The costs to climate and biodiversity of its destruction are invisible to markets. What isn't priced isn't valued. What isn't valued gets destroyed.

Fining parents for lateness made them later — money crowds out duty

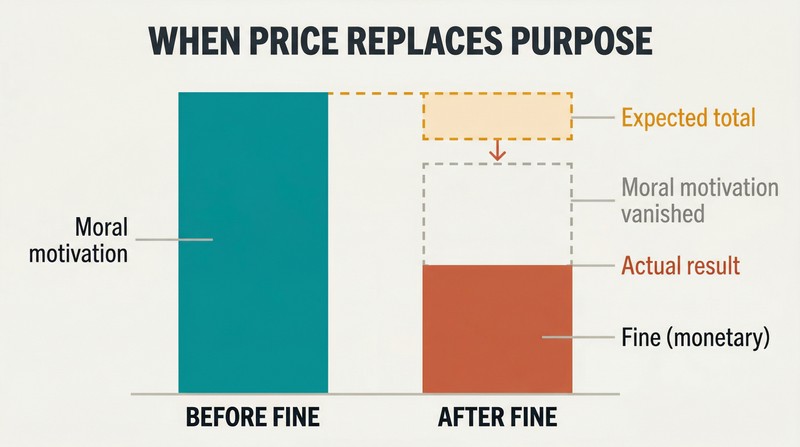

Putting a fee on a moral obligation transforms it into a transaction. At an Israeli day-care center, fines for late pickup caused lateness to increase — parents treated the fine as a price, removing the social stigma of inconveniencing teachers. Richard Titmuss showed the UK's voluntary blood-donation system outperformed America's paid one. In a fundraising experiment, students motivated purely by charitable purpose raised more money than those offered a 1% commission.

Carney calls this the commercialisation effect: commodifying a good can corrode its character. Standard economics assumes pricing an activity adds monetary incentive on top of existing moral motivation. The evidence shows these motives are often substitutes, not complements — and the monetary one can extinguish the moral one entirely.

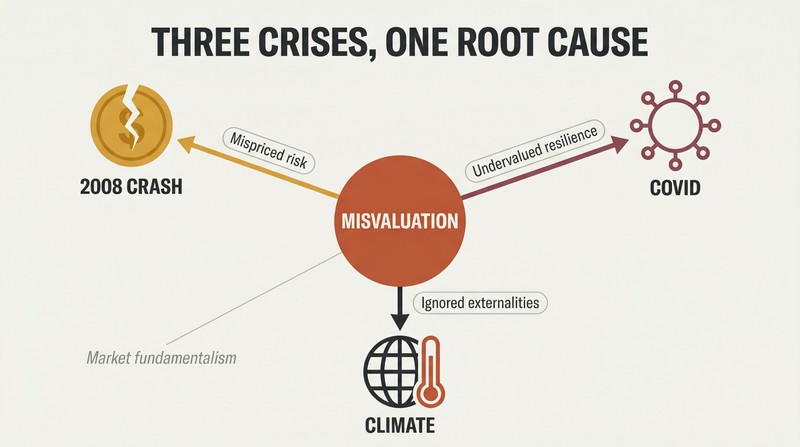

The 2008 crash, Covid, and climate share one root cause: misvaluation

Three defining crises, one pattern. The financial crisis arose from misvaluing risk — light-touch regulation, the delusion that securitization had eliminated danger, and banks deemed too big to fail operating in a 'heads I win, tails you lose' bubble. The Covid catastrophe arose from undervaluing resilience — governments ignored warnings, depleted stockpiles, and left pandemic plans unfinanced. The climate emergency persists because we don't price carbon externalities or weigh the welfare of future generations.

In each case, market fundamentalism — the faith that the market is always right and that adding more markets solves market failures — obscured catastrophic risks. The $15 trillion in bailouts after 2008, the trillions lost to Covid, and the looming costs of unchecked warming are all invoices for what markets failed to value.

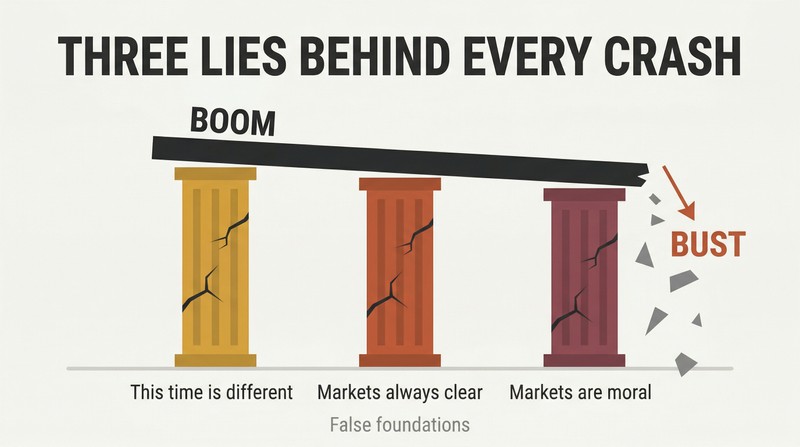

Three seductive lies fuel every financial boom-and-bust

Carney identifies three recurring delusions behind eight centuries of financial crashes:

1. "This time is different" — complacency bred by success (the Great Moderation before 2008)

2. "Markets always clear" — faith that prices are always right, so bubbles can't exist (Greenspan's doctrine)

3. "Markets are moral" — assuming self-interest naturally maintains integrity

The 2008 crisis proved all three false. Global bank misconduct costs exceeded $320 billion — capital that could have supported $5 trillion in lending. Only 20% of UK citizens trusted banks afterward, down from 90% in the 1980s. Post-crisis reforms raised bank capital requirements tenfold, but Carney warns these gains vanish if we fall back under the spell of the same three lies.

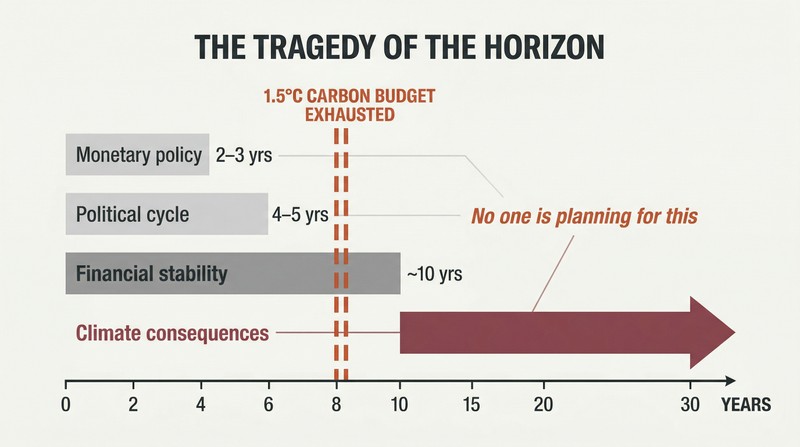

Climate catastrophe falls beyond every decision-maker's planning window

Carney coined 'the tragedy of the horizon' to describe climate change's unique temporal trap. Monetary policy looks out 2 – 3 years. Financial stability horizons stretch to a decade. Political cycles run 4 – 5 years. But the carbon budget for limiting warming to 1.5°C could be exhausted within roughly eight years at current emission rates. By the time climate becomes the defining issue for any decision-maker, it may be too late.

The numbers are stark. A child born today has a lifetime carbon budget one-eighth of their grandparents'. To stay at 1.5°C, emissions must fall 8% annually — even the Covid lockdowns achieved only 5 – 7%. To meet the Paris target, over 80% of known fossil fuel reserves must stay in the ground. Yet most companies that disclose a shadow carbon price use a static, backward-looking figure well below the $50 – $120/tonne needed.

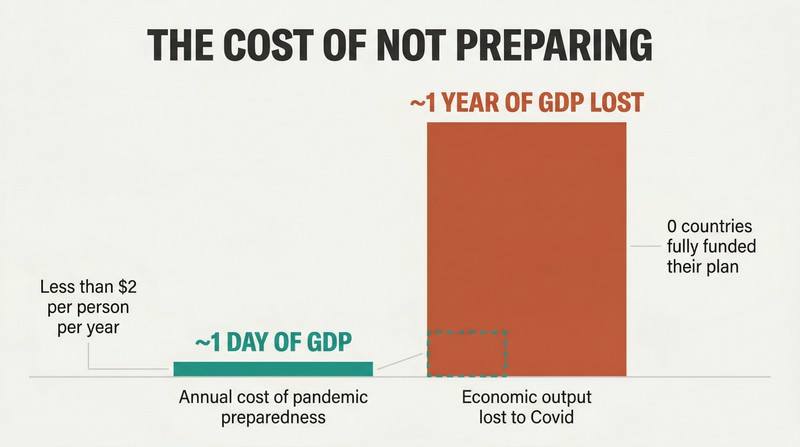

Annual pandemic prep cost one day of the GDP we ultimately lost

Governments failed their most fundamental duty: protection. The World Bank estimated improving pandemic preparedness in poorer countries would cost less than $2 per person per year. Even doubling that globally would amount to roughly one day of the economic output lost to Covid. Yet not a single country fully financed its pandemic action plan before the virus hit. The US mask stockpile covered approximately 1% of what a severe pandemic required.

South Korea was the exception. After its 2015 MERS outbreak, it reformed testing and contact tracing laws — and contained Covid without ever imposing a full lockdown. Elsewhere, cognitive biases — present bias, confirmation bias, disaster myopia — systematically led governments to divert preparedness funding. Notably, the Global Health Security Index ranked the US and UK first and second in preparedness; both fared poorly, while low-ranked New Zealand succeeded through state legitimacy and social trust.

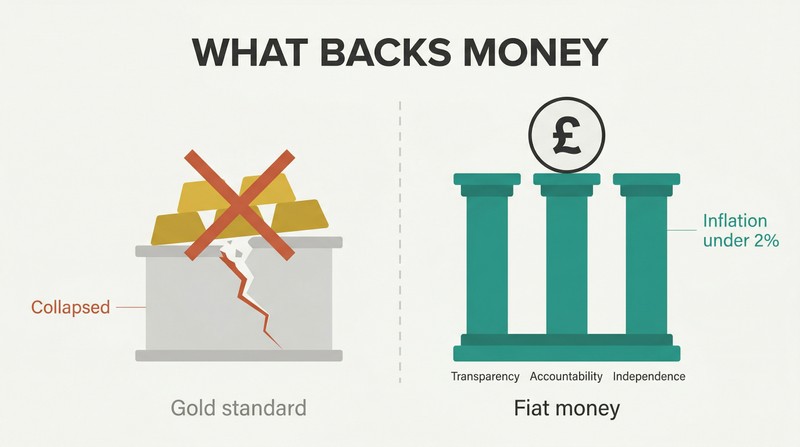

Gold is a relic — money runs on trust, transparency, and accountability

5,500 tons of gold sit uselessly in the Bank of England's vaults — a vestige of a system that collapsed because its values conflicted with society's. The gold standard demanded wage cuts and unemployment to maintain currency pegs, burdens that fell hardest on workers with no political voice. Once suffrage expanded and labor organized, the system lost legitimacy and broke down.

Modern fiat money works because independent central banks operate under constrained discretion — clear mandates, transparent decisions, and democratic accountability. Since the Bank of England gained independence in 1998, inflation averaged just under 2% versus over 6% before. The Magna Carta's constitutional legacy — delegated authority with limits and answerability — underpins this architecture. As Carney discovered when he corrected a tour guide: the Bank's money is backed not by gold but by credible monetary policy. The bus never returned.

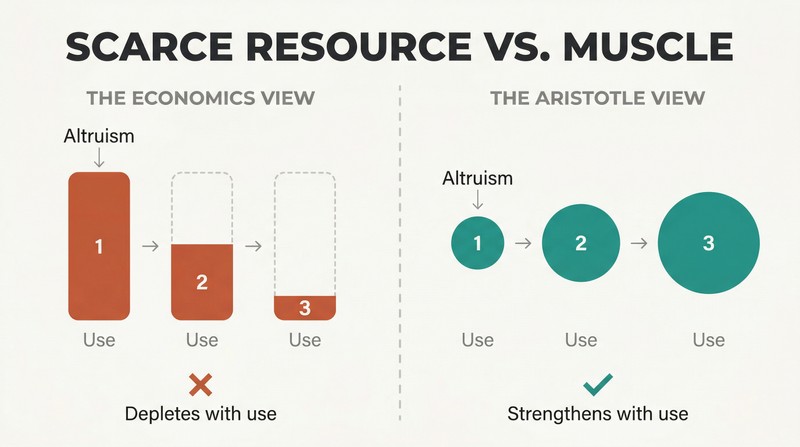

Altruism isn't a scarce resource to ration — it strengthens with use

Mainstream economics gets this backwards. Nobel laureate Kenneth Arrow argued in 1972 that ethical behavior should be 'economised' like any scarce commodity. But extensive evidence shows that public spiritedness increases, not decreases, with practice. Aristotle saw this clearly: 'We become just by doing just acts, temperate by doing temperate acts, brave by doing brave acts.'

Covid proved the point at scale. The UK's appeal for NHS volunteers drew over a million people within days — unpaid. Voluntary community groups made PPE without compensation. Citizens helped elderly neighbors without government programs. Conversely, when we outsource civic duties to paid third-party providers, we narrow the scope of community and encourage withdrawal from it. The expansion of the market into family and civic life — from paid child-rearing to commodified essay-writing — steadily erodes the social capital that markets themselves require to function.

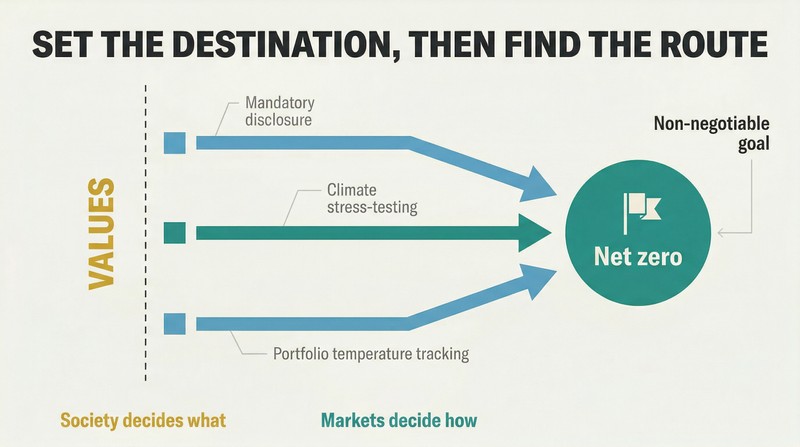

Let society's values set the destination; let markets find the route

For existential challenges, Carney argues for cost-effectiveness analysis over cost-benefit analysis. In crude cost-benefit analysis, everything — including human life — gets a monetary value, and decisions are made on the margin. In cost-effectiveness analysis, society first sets the goal based on its values (R0 below 1 for Covid, a carbon budget for 1.5°C), then examines the cheapest policies to achieve it.

During Covid, populations rejected the utilitarian calculus. People acted as Rawlsians — prioritizing the vulnerable — not as libertarians optimizing individual liberty. This revealed preference should guide climate policy too. Over 125 countries have set net-zero targets. The practical agenda is to make every financial decision take climate into account through mandatory disclosure (TCFD ), climate stress-testing of banks, and measuring every investment portfolio's 'implied temperature rise.' Credible policy makes the transition cheaper — just as a credible central bank needs smaller interest rate moves.

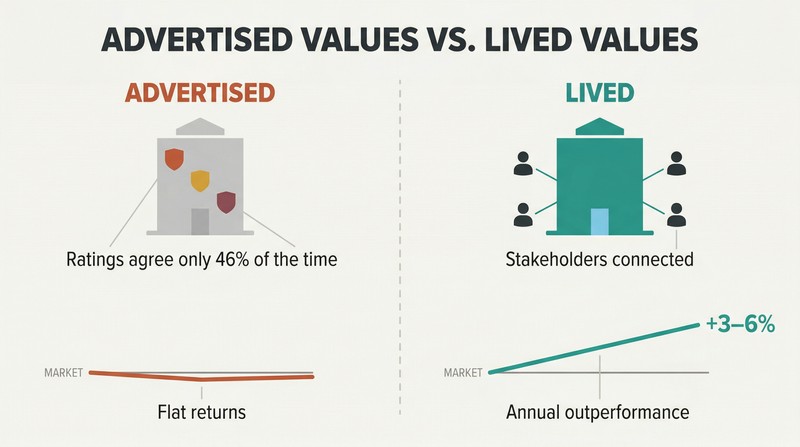

Companies solving stakeholder problems outperform the market by 3 – 6%

Purpose isn't soft — it's measurable. A meta-analysis of 2,200+ studies found 90% reported a non-negative link between ESG criteria and financial performance. Companies investing heavily in ESG issues material to their industry outperformed the market by 3 – 6% annually. During the 2008 crisis, high-CSR firms posted stock returns 4 – 5% above low-CSR peers. Patagonia gets 9,000 applications per internship.

But ESG is not a magic label. Six leading ESG ratings providers agree on company scores only 46% of the time — investors who outsource judgment to ratings without understanding the methodology are flying blind. Carney argues that shareholders aren't even owners in the legal sense (a 1948 UK Court of Appeal ruling confirmed this), undermining shareholder-primacy doctrine. The 2019 Business Roundtable statement — 181 CEOs endorsing stakeholder capitalism — signals the tide turning, but values 'advertised on websites' don't improve performance. Only values noticed and lived by employees do.

Analysis

Mark Carney occupies an almost unique vantage point in modern political economy: the only person to have governed two G7 central banks (Canada and England), chaired the Financial Stability Board during its post-crisis reform period, and served as UN Special Envoy for Climate Action. This institutional pedigree gives Values a concreteness that distinguishes it from purely academic critiques of market fundamentalism by scholars like Michael Sandel or Mariana Mazzucato, whose arguments Carney explicitly builds upon.

The book's most original intellectual contribution is the 'tragedy of the horizon '— the insight that climate change's catastrophic impacts will materialize beyond the temporal horizons of virtually every decision-making institution. This framing, which Carney introduced in a 2015 speech at Lloyd's of London, has become canonical in climate finance. Its power lies in diagnosing the problem as structural, not moral: even well-intentioned actors face incentive structures that discount the future catastrophically.

Carney's central tension — that markets are simultaneously humanity's greatest problem-solving engine and a corrosive force on the social capital they require — is more honest than most treatments from either the pro-market or anti-market camps. His resolution, 'mission-oriented capitalism' where society sets values-based goals and markets discover solutions, echoes Mazzucato's mission-oriented innovation but adds institutional detail from someone who has actually built the TCFD disclosure framework and implemented the Senior Managers Regime.

The book's weakness is its ambition. At 191,000 words spanning Aristotle to blockchain to Canadian childcare policy, it sometimes reads like the memoirs, manifesto, and policy white paper of three different books. The Canada-specific chapter feels parochial after the global sweep. And the prescriptive framework — seven values, ten-point national plans — occasionally lapses into the bureaucratic. Yet the core argument that subjective value theory, left unchecked, corrodes the very moral sentiments on which Smith built his case for markets, is both intellectually rigorous and urgently relevant.

Review Summary

Value(s) by Mark Carney receives mixed reviews. Many praise its thoroughness and thought-provoking ideas on economics, finance, and social values. Readers appreciate Carney's insights on crises like the 2008 financial crash, COVID-19, and climate change. However, some find the book overly long, dense, and repetitive. Critics note its heavy use of financial jargon and occasionally self-aggrandizing tone. While some reviewers find it enlightening, others struggle with its complexity and length. Overall, the book is seen as ambitious but challenging for general readers.

People Also Read

Glossary

Tragedy of the horizon

Climate falls beyond planning windowsA concept coined by Carney to describe how the catastrophic impacts of climate change will be felt beyond the traditional planning horizons of most business leaders (3-5 years), investors (up to 10 years), and politicians (electoral cycles). By the time climate becomes a defining issue for these decision-makers, it may be too late to prevent its worst effects. The concept highlights a structural — not moral — failure in how institutions discount the future.

Market society

Markets governing all of lifeCarney's term (building on Michael Sandel) for the shift from a market economy — where markets are tools for organizing productive activity — to a society where market logic, buying, and selling govern virtually all domains of life, including healthcare, education, civic duties, and personal relationships. In a market society, what isn't priced is treated as valueless, and the act of pricing changes social norms and moral sentiments.

Three lies of finance

Delusions behind every financial crisisCarney's framework identifying three recurring beliefs that precede financial crises: (1) 'This time is different' — complacency from sustained prosperity; (2) 'Markets always clear' — the assumption that prices are always right and bubbles cannot be identified; and (3) 'Markets are moral' — the belief that self-interested market participants will naturally maintain system integrity. These delusions drove the pre-2008 boom and have recurred across eight centuries of financial history.

Constrained discretion

Delegated authority with accountability limitsThe governance model under which modern central banks operate: they receive specific mandates from elected governments (such as an inflation target), have operational independence to pursue those mandates using their tools, but are accountable to Parliament and the public for their performance. Carney traces this principle from the Magna Carta's constraints on royal authority to the Bank of England Act 1998, arguing it resolves the 'time inconsistency' problem where politicians are tempted to sacrifice long-term price stability for short-term growth.

TCFD

Climate financial disclosure frameworkThe Task Force on Climate-Related Financial Disclosures, established by the FSB in 2015 under the leadership of Michael Bloomberg. The TCFD developed voluntary recommendations for companies to disclose climate-related financial risks covering governance, strategy, risk management, and metrics. Adopted by over 1,300 companies and supported by financial institutions controlling $170+ trillion in assets. Its signature innovation is requiring scenario analysis — forward-looking stress tests of business models under different climate pathways.

Senior Managers Regime

Personal accountability for bank executivesA UK regulatory framework introduced after the financial crisis that holds the most senior banking executives individually accountable if they fail to take reasonable steps to prevent regulatory breaches in their areas of responsibility. Key features include deferred compensation for up to seven years, clawback provisions for misconduct, regulatory references that follow employees between firms, and annual fitness-and-propriety certifications. Carney opposed the EU's bonus cap, arguing that reducing at-risk pay actually blunts accountability.

Commercialisation effect

Pricing changes the good's characterThe phenomenon whereby introducing a monetary price for a good, service, or activity changes its fundamental nature by crowding out intrinsic motivations like moral conviction, civic duty, or personal interest. Documented examples include day-care fines increasing lateness (by converting stigma into a fee), paid blood donation reducing supply quality (by undermining altruism), and financial incentives reducing charitable fundraising effectiveness. Contradicts the standard economic assumption that monetary incentives are always additive.

Minsky moment

Sudden collapse after complacency-driven excessNamed after economist Hyman Minsky, this describes the point at which an extended period of stability and rising asset prices (which encourages increasingly speculative borrowing) suddenly reverses as lenders and investors simultaneously reassess risks. Carney applies the concept broadly: to the 2008 financial crisis (when subprime assumptions collapsed), and prospectively to climate change (a 'climate Minsky moment' when markets suddenly reprice stranded fossil fuel assets). The cycle runs: prudence → confidence → complacency → euphoria → despair.

Dynamic materiality

ESG relevance shifts over timeThe concept that the importance of specific environmental, social, and governance factors for a company's financial performance can change rapidly as societal norms evolve, regulations shift, or physical risks intensify. Before carbon budgets were quantified, environmental sustainability concerned mainly energy companies; now it affects every sector. Dynamic materiality explains why static ESG scores may miss emerging risks and why companies must track evolving standards of social licence rather than simply reporting current compliance.

Cooperative internationalism

Outcomes-based, flexible global cooperationCarney's proposed alternative to rules-based multilateralism for a world where binding global agreements are increasingly difficult. Modeled on the Financial Stability Board's post-crisis reform process, cooperative internationalism is outcomes-based (not rules-based), involves flexible coalitions rather than universal membership, is interoperable across different political systems, and builds consensus through shared analysis rather than treaty obligation. Countries implement standards voluntarily based on shared ownership, not legal compulsion.

FAQ

What's Values: Building a Better World for All about?

- Exploration of Value and Values: The book examines the relationship between economic value and societal values, arguing that market prices often overshadow deeper ethical considerations.

- Market Society Critique: Mark Carney critiques the shift from a market economy to a market society, where everything is commodified, leading to a crisis in values.

- Call for Change: The author advocates for rebalancing values to ensure economic systems serve humanity, emphasizing solidarity, responsibility, and sustainability.

Why should I read Values: Building a Better World for All?

- Timely Relevance: The book addresses pressing global issues like climate change, economic inequality, and the COVID-19 pandemic, making it highly relevant today.

- Expert Perspective: As a former central banker, Carney offers a unique perspective on the intersection of economics and ethics, lending credibility to his arguments.

- Practical Solutions: It provides actionable insights for leaders, companies, and individuals on creating a more inclusive and sustainable economy.

What are the key takeaways of Values: Building a Better World for All?

- Value vs. Values: Carney emphasizes the distinction between market value and societal values, arguing that the former should not overshadow the latter.

- Importance of Trust: Trust in institutions and the financial system is crucial for maintaining economic stability and societal wellbeing.

- Need for Inclusive Growth: Carney advocates for a social contract that promotes equality of opportunity and outcomes, ensuring economic growth benefits all.

What are the best quotes from Values: Building a Better World for All and what do they mean?

- "Value is built on values.": This encapsulates the book's thesis that economic value is intertwined with ethical and moral values.

- "The market is humanity distilled.": Carney illustrates how markets reduce complex human values to transactions, urging a holistic understanding of value.

- "We cannot take the market system... for granted.": A reminder that markets must be aligned with societal values to function effectively.

How does Mark Carney define "value" in Values: Building a Better World for All?

- Value as Importance: Carney defines value as "the regard that something is held to deserve," emphasizing its societal importance.

- Subjective Nature: He discusses how value is often equated with monetary value, leading to a narrow understanding of true worth.

- Connection to Values: Our perceptions of value are deeply influenced by the values we hold, shaping judgments about importance.

What is the "tragedy of the horizon" mentioned in Values: Building a Better World for All?

- Long-term Risks: Carney describes the tendency to prioritize short-term gains over long-term sustainability, especially in climate change.

- Intergenerational Equity: It highlights the moral failure to address issues impacting future generations, like environmental degradation.

- Call for Action: Recognizing this tragedy is essential for creating policies that ensure a sustainable future.

How does Values: Building a Better World for All propose to reclaim our values?

- Values-Based Leadership: Carney emphasizes leaders who embody values like integrity, fairness, and responsibility.

- Purposeful Companies: Companies aligning business models with societal values can create long-term value for stakeholders.

- Investment in Social Capital: Investing in social capital is crucial for rebuilding trust and community.

What role does money play in shaping values according to Values: Building a Better World for All?

- Measurement of Value: Money serves as a unit of account, allowing measurement and comparison of goods and services.

- Trust and Confidence: The value of money is grounded in public trust, essential for economic stability.

- Social Convention: Money is a social construct, with its value determined by societal values and beliefs.

How does Values: Building a Better World for All address the future of money?

- Central Bank Digital Currencies (CBDCs): Carney discusses CBDCs as a stable digital money form enhancing financial inclusion.

- Private Innovations: Innovations like cryptocurrencies can complement public money while ensuring stability and trust.

- Balancing Innovation and Regulation: A regulatory framework is needed to support financial innovation while safeguarding sound money values.

What specific methods does Mark Carney suggest for improving economic systems in Values: Building a Better World for All?

- Reinforcing Core Values: Initiatives promoting fairness, integrity, and responsibility within economic systems are suggested.

- Integrating Non-Priced Attributes: Incorporating attributes like mental health and dignity into economic assessments is advocated.

- Encouraging Altruism and Solidarity: Fostering a culture of altruism and community engagement can enhance social capital.

How does Values: Building a Better World for All relate to climate change?

- Climate as a Crisis of Value: Carney argues that market failure to account for environmental costs leads to unsustainable practices.

- Call for Collective Action: Emphasizes aligning individual and corporate responsibilities with societal values for climate action.

- Integration of Climate Goals: Economic systems should integrate climate goals, considering long-term environmental impacts.

What is the significance of net-zero transition in Values: Building a Better World for All?

- Urgent Necessity: Achieving net-zero emissions is critical for combating climate change and ensuring sustainability.

- Investment Opportunities: The transition presents significant investment opportunities, encouraging support for decarbonization plans.

- Framework for Assessment: Metrics for assessing progress towards net-zero goals emphasize transparency and accountability.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.